LNG is seen as both a bridge to a low-carbon future and a foundation for meeting rising global energy demand, ensuring system reliability, and supporting climate goals.

What is LNG ?

Natural Gas is a safe, efficient, clean and reliable energy.

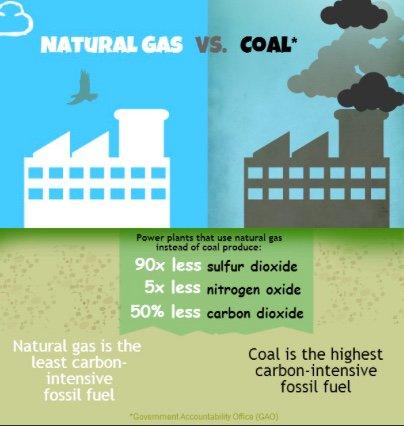

LNG (Liquefied natural gas) is natural gas in its purified and liquefied form. It is the cleanest burning fossil fuel and it creates up to 45% fewer emissions than coal and oil. Natural gas consists mainly of methane with low concentrations of other hydrocarbons (ex: ethane, propane and butane).

LNG Characteristics

Natural gas is odorless, non-pressurized, non-corrosive and non-toxic.

Natural gas is cooled to -160° Celsius where the gas becomes liquid and natural gas in a liquid state (referred as LNG) occupies 1/600 of its original volume. Therefore, LNG can be stored in tanks and loaded easily into ISO Containers or into LNG carriers for safe and efficient shipment across the world.

Natural gas is delivered by pipelines, by vessels, by cryogenic tanks and by trucks to millions of homes and businesses across the world and the LNG industry has an excellent global safety record. Many countries such as India, South Korea and China are increasing their imports and consumption of natural gas every year.

LNG is a bridge between fossil fuels and renewable energy.

LNG News & Canadian LNG Projects: Click here to see the latest Canadian and global LNG developments, including projects, exports, policies, market trends, and an in-depth article on the history, current projects, future outlook, and challenges of Canadian LNG.

Use of LNG

Liquefied Natural Gas is used in the residential sector for cooking and heating purposes and LNG is also used in various industries including:

- Construction

- Manufacturing

- Food Processing

- Mining

- Marine

- Oil & Gas

- Power Generation

- Transportation

LNG is used as an alternative fuel in various mode of transports such as rails, ships, trucks and natural gas vehicles.

LNG Market

The global LNG market is expected to grow in the coming decades with the growing population, the increase of energy consumption, the accelerating economic growth and the increasing preference of cleaner energy in developing economies. Based on many analysis, China will become the world’s top importer of natural gas natural gas from 2019 and the demand has been driven by policy to move to cleaner burning energy source and to help the Country achieve his ambitious air quality targets.

The main exporters of LNG are Australia, Qatar and the USA and the main importers are Japan, South Korea, China and Europe. The LNG is transported using large cryogenic tankers that can carry up to 266,000 cubic metres of LNG (approx 121000 tons).

International Energy Agency says that the demand in China for LNG is expected to rise by 60% between 2017 and 2023 and despite the huge increase in LNG imports in China in the past few years, there are still fears of a gas shortage in the next decade if no new investments are made in production and in adequate storage. LNG is a clean fuel and Companies in China that are switching to natural gas are helping to improve the air quality and to reduce CO2 emissions greatly.

Click here to see a list of the top producing countries of natural gas.

The export of LNG from Canada could facilitate Canadian natural gas production growth and also result in significant economic growth for the Country.

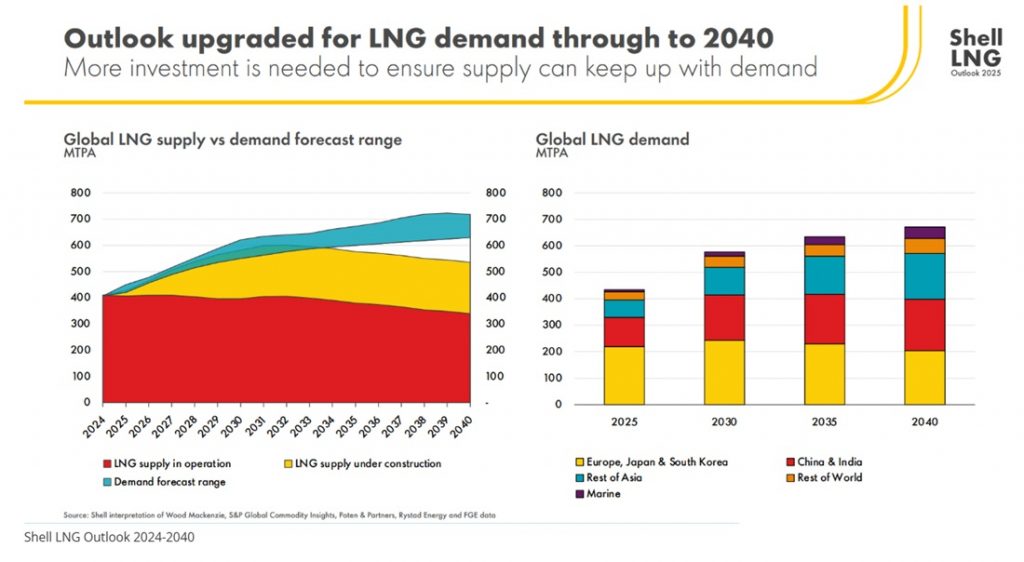

LNG Global Markets

Demand Outlook through 2040

Source: Shell

LNG Value Chain

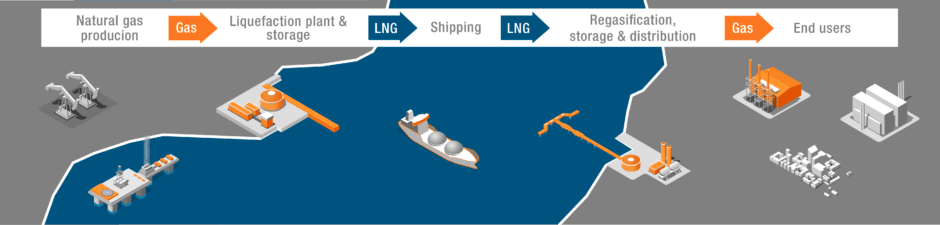

An LNG supply chain consists of five main activities:

- Exploration and Production of natural gas (Extraction of natural gas).

- Treatment (The process includes removing liquids, solids, vapours and impurities).

- Liquefaction of natural gas into LNG (convert the natural gas into liquid form which reduces its volume for easy transportation purposes).

- Shipping of LNG (After liquefaction, LNG is loaded onto specially designed ships or into ISO containers to keep the LNG in liquid state during the transportation to the final destination).

- Receiving, Storage and Distribution (An LNG receiving terminal comprises LNG storage tanks and regasification facilities that convert LNG back to its ”gaseous” state for distribution to end-users).

* LNG that is imported in ISO Tank Containers can be moved directly by truck from the LNG Liquefaction plant, then shipped by container cargo and moved by truck once it arrives at the destination port.

LNG can be transported by pipeline, by trucks, by LNG vessels and in Cryogenic ISO Tank Containers.

LNG Tankers

Once the tanker reach the dedicated import terminal, the Liquefied Natural Gas is stored in large storage tanks and compressed and vaporized for injection into the gas transmission grid.

Most LNG import terminals also have truck loading facilities where the product can be loaded on specialized trailers and containers for the distribution to customers and end-users. LNG enables cost competitive long distance transport of natural gas and it can also be easily transported in ISO tank conatiners to any ports that accepts DG. The volumes that are distributed by containers represent a small fraction of the total LNG imports but the demand for LNG is growing fast.

LNG ISO Containers

The LNG that is distributed by ISO containers can be used in a wide range of applications (ex: industrial processes, power plants, road and marine transport, etc.)

and the transportation can be applied over long distances and through the traditional sea routes using container ships. Therefore, it enables a cost competitive fuel supply to end-users and it also brings some flexibility to importers, distributors and traders who don’t have access to LNG import terminals and/or financial capacity to buy a whole cargo.

LNG Virtual Pipeline

The LNG can be move easily from a small-scale LNG Plant or refilling station to the end user by using LNG ISO containers. Transportation mode by land (truck), sea (standard containers vessel) and rail. Click here to learn more about LNG-to-Power solutions.

Traditional Supply Chain

The standard LNG supply chain requires large LNG receiving terminals, onshore storage tanks and LNG carriers to move the product from a producing Country to the destination port/receiving terminal.

Canada LNG

History, Trends & Future Outlook

Canada’s liquefied natural gas (LNG) industry has entered a new chapter in 2025, marking its entry as a major exporter on the global stage. While the country has long been rich in natural gas resources, it has only recently built infrastructure to turn that gas into exportable LNG. The industry is now evolving rapidly, driven by large-scale projects, low-carbon ambition, and increasing demand from Asia.

As the world pivots to cleaner and more secure energy supplies, Canadian LNG is emerging as a powerful, competitive, and responsible player.

2025 is a Milestone Year

First Exports and Operational Scale

In June 2025, LNG Canada made history by loading its first export cargo from its Kitimat, British Columbia terminal. The facility, a joint venture between Shell, Petronas, PetroChina, Mitsubishi, and KOGAS, is structured with two processing units (“trains”) and a total capacity of 14 million tonnes per annum (Mtpa). LNG Train 1 began production earlier in 2025.

By November 2025, LNG Canada announced that its second train (Train 2) was brought online, increasing its export potential. This expansion is strategically important: the Kitimat plant provides Canada with deepwater access to Pacific shipping routes — significantly reducing transport time to major Asian markets compared to Gulf Coast U.S. terminals.

What are the LNG Projects in Canada ?

Beyond LNG Canada, several high-profile LNG projects are shaping the industry’s future direction.

One such project is Cedar LNG, a floating LNG (FLNG) facility in Kitimat, which is majority-owned by an Indigenous nation. When complete, it is expected to produce around 3.3 Mtpa of LNG. Importantly, the facility is designed to use hydroelectric power to minimize its carbon footprint, positioning it as one of the cleanest LNG projects globally.

Another major initiative is Woodfibre LNG, located near Squamish, B.C. This project is targeting around 2.1 Mtpa of export capacity and is designed with environmental considerations in mind, including minimizing emissions and working closely with local First Nations communities.

LNG Canada is a landmark liquefied natural gas export facility located in Kitimat, British Columbia, jointly owned by Shell, PETRONAS, PetroChina, Mitsubishi, and KOGAS. The project officially began exporting in June 2025, with a long-term export license enabling up to 14 Mtpa via two liquefaction trains. It is considered one of Canada’s most significant private-sector investments, and its coastal location offers a direct route to growing Asian markets. The facility is expected to operate for decades, fostering economic development in B.C., involving strong community partnerships, and serving as a critical node in Canada’s energy export infrastructure.

Flowing underneath these projects is a broader pipeline and infrastructure build-out, notably the Coastal GasLink pipeline that enables supply to Kitimat. Several other export proposals are under review, including concepts such as Ksi Lisims LNG, Tilbury LNG, and Summit Lake, which together could significantly expand Canada’s export capacity.

What are the LNG Market Trends & Strategic Drivers for Canadian LNG

Asian Demand & Strategic Export Routes

Canada’s LNG exports are increasingly aligned with Asian demand. With its Pacific coast access, Canada is well-positioned to serve key Asian markets, which remain among the largest and fastest-growing purchasers of LNG. The country’s export strategy is being viewed as both economically and geopolitically strategic.

Low‑Carbon LNG Ambitions

One of the defining stories of Canada’s LNG future is its low-carbon ambition. Cedar LNG, with its Indigenous majority ownership, is designed to be powered by clean hydroelectricity, dramatically lowering its emissions profile. This aligns with broader global trends toward cleaner energy production and may give Canadian LNG a competitive advantage in markets that value environmental credentials.

Regulatory & Licensing Support

Long-term export licences (e.g., up to 40 years) have been granted for some LNG projects, giving developers and investors confidence in Canada’s long-term export strategy. The government has also made financial and regulatory support available to ensure project viability, especially for projects that combine economic development with environmental stewardship.

Indigenous Participation & Community Impact

The Cedar LNG project is a pioneering example of Indigenous ownership and partnership in major energy infrastructure. This model supports economic reconciliation and ensures that energy development aligns with the values of local communities. It also demonstrates how LNG export projects can be both commercially viable and socially inclusive.

Economic and Energy Transition Benefits of Canadian LNG

LNG development in Canada brings significant economic and energy transition benefits, including the creation of high-value jobs, infrastructure investment, and export revenues that strengthen the national economy. Canadian LNG supports energy security and independence while supplying global markets with lower-carbon natural gas, helping other countries reduce reliance on more carbon-intensive fuels.

At the same time, the industry acknowledges that not everyone views LNG as climate-friendly, and concerns about greenhouse gas emissions and environmental impacts are valid. Fortunately, ongoing innovations such as carbon capture and storage, methane leak reduction, and integration of blue and green hydrogen are helping reduce LNG’s climate footprint. By combining responsible practices with technological advancement, Canadian LNG has the potential to contribute to both economic growth and a cleaner global energy mix.

Challenges for Canada LNG

Canada’s LNG ambitions are not without risk. The ramp-up of operations at the Kitimat terminal has faced technical challenges, potentially limiting output in the near term. Moreover, natural gas prices in Western Canada remain under pressure, as supply outpaces domestic demand and export routes are still new.

Despite the momentum, the Canadian LNG industry faces several key challenges in 2026 and beyondé

- Ramp-up issues: While Train 2 of LNG Canada is now operational, Train 1 has reportedly faced technical issues, limiting its output.

- Low gas prices: Oversupply and pipeline constraints in Western Canada have pressured natural gas prices, which could affect the economics of LNG projects.

- Capital intensity: Building large LNG facilities is expensive, and future phases depend on securing sufficient financing, regulatory approvals, and long-term offtake agreements.

- Environmental scrutiny: As LNG production grows, stakeholders are closely watching emissions, water use, and community impact. Achieving environmental and social benchmarks will remain critical for new projects.

What to Expect in 2026 and Beyond

Expansion & Growth

Looking forward, the phase‑2 expansion of LNG Canada could double its capacity — a move that would significantly increase Canada’s export footprint. Other projects, like Ksi Lisims and Tilbury LNG, are progressing through planning and investment stages, but their success will depend on regulatory approvals and securing long-term contracts.

Export Leadership

With its strategic geography and advanced infrastructure, Canada stands to become a reliable low-carbon LNG supplier for Asia and beyond. This could reshape global LNG trade flows and challenge incumbent exporters.

Sustainability as a Differentiator

Canada’s LNG projects may increasingly compete on the basis of emissions credentials. Projects that minimize carbon intensity, incorporate Indigenous ownership, and offer long-term sustainability will attract both public and private capital.

Capital & Partnerships

To unlock future capacity, developers will rely on global capital, joint ventures, and blended financing. The involvement of institutional investors, sovereign funds, and energy companies will be critical to advancing new phases and greenfield projects.

Canada’s coastal location gives it a growing advantage in the global LNG trade, particularly toward Asia. By combining scale with sustainability, Canadian LNG could become a supply source of choice for countries pursuing energy security and lower emissions.

Increasingly, financial and industrial partners are aligning around these goals. Global capital — including infrastructure funds, energy companies, and institutional investors — is expected to play a major role in funding the next wave of Canadian LNG infrastructure.

A Global Energy Transition Story

The LNG industry in Canada is not just another energy story, it’s a global energy transition story. With its abundance of natural gas, strategic geography, and commitment to low-carbon development, Canada is emerging as a new force in LNG exports.

For project developers, investors, and capital providers, Canada offers a compelling combination:

- Strategic Pacific export position

- Low-carbon production plans

- Indigenous collaboration and partnerships

- Long-term regulatory certainty

Canada’s LNG sector could be one of the most important growth stories of the next decade.

About the Global LNG Trade

In 2024, global LNG trade grew by 2.4%, reaching 411 million tonnes (MT). Trade now connects 22 exporting markets with 48 importing markets. Asia-Pacific remains a major player, with strong demand growth, while European LNG imports declined slightly due to high storage levels and continued pipeline gas flows.

Long-Term Demand Outlook

Global LNG demand is expected to reach between 630 and 718 million tonnes per year by 2040, representing approximately a 60% rise from current levels. Growth is driven by industrial demand, coal-to-gas switching in Asia, and increasing use of natural gas for power, transport, and heavy industry. LNG continues to play a vital role as a flexible, lower-emission transition fuel toward renewable energy.

Liquefaction Capacity

Global liquefaction capacity reached approximately 494 MTPA by the end of 2024. Capacity growth has been driven by expansions in the U.S., new floating liquefaction projects, and other global developments. However, the volume of new projects reaching Final Investment Decision remains limited, highlighting the need for careful planning to meet future demand.

Market Balance & Risks

The LNG market is currently in a fragile equilibrium. Limited spare supply and project delays may impact future trade. Geopolitical risks, regulatory hurdles, and slower-than-expected infrastructure ramp-up are key factors affecting supply growth.

Pricing & Trade Dynamics

Spot LNG prices remain volatile, influenced by demand spikes, especially in Asia, and limited inventory. LNG is increasingly used as a cleaner alternative to more polluting fuels, particularly in shipping, power generation, and industrial sectors.

Opportunities for Flexible LNG Solutions

The long-term demand outlook supports growth in flexible LNG supply solutions, including LNG containers and small-scale or modular systems. Industrial users and power producers are increasingly seeking cleaner, flexible fuel options.

At Canada LNG Group, we are confident that LNG will continue to play a central role in the global energy transition, offering strong opportunities for projects that are well-planned, technically sound, and backed by suitable financial partners.

LNG Pricing Overview

Spot LNG Cargoes

Spot LNG prices are determined by short-term market conditions and vary by region:

- Asia: The Japan Korea Marker (JKM) is the benchmark for LNG delivered to Northeast Asia. Prices reflect current supply-demand dynamics, seasonal demand, and shipping availability.

- Europe: The Title Transfer Facility (TTF) is the main benchmark for European LNG, tracking natural gas prices at key European hubs.

Long-Term LNG Offtake Agreements

Long-term LNG contracts typically use formula-based pricing to provide stability for both buyers and sellers:

- Henry Hub-linked Contracts: Prices are often calculated as Henry Hub + liquefaction fee + shipping cost, sometimes with a markup (e.g., +10–15%).

- Oil-linked Contracts: Some agreements use a slope against Brent Crude or other oil benchmarks, where the LNG price is tied to a percentage of oil prices over a defined period.

These formulas ensure that LNG pricing reflects regional market conditions, production costs, and long-term supply security, balancing flexibility and predictability for buyers and sellers alike.

Long-Term LNG Pricing Formula (USA, Canada)

Price = Henry Hub Price + Fixed Liquefaction Fee

Components:

- Henry Hub Price: The spot price of natural gas at Henry Hub, Louisiana, a major US trading hub.

- Fixed Liquefaction Fee: A per-MMBtu fee for liquefaction services, fixed and not subject to market fluctuations.

- Take-or-Pay Component: Buyers are required to pay the fixed fee for a contracted volume even if they do not take the cargo. This ensures liquefaction and production costs are covered, separate from the variable cost of the gas itself.

This formula illustrates how long-term LNG contracts balance variable gas costs with stable liquefaction and shipping fees, providing predictability for both sellers and buyers.

Global LNG & Gas Prices

- Global gas prices have remained volatile, influenced by supply-demand dynamics, seasonal variations, and geopolitical factors.

- In 2024, Asian spot LNG prices averaged around $11–$13/mmBtu, reflecting higher demand and tight supply.

- Henry Hub (USA) natural gas prices averaged approximately $3–$4/mmBtu in 2024.

- More than 1,800 LNG cargoes were traded globally in 2024, highlighting the continued growth and liquidity in the LNG market.

Liquefaction Plants

- Global LNG liquefaction capacity reached approximately 494 MTPA by the end of 2024.

- Capacity growth has been driven by expansions in the United States, new floating liquefaction (FLNG) projects, and other international developments.

- Despite growing capacity, new project Final Investment Decisions (FIDs) remain limited, emphasizing the importance of strategic planning to meet future LNG demand.

LNG Shipping

- The global LNG fleet now consists of over 5,500 active vessels, including FSRUs (Floating Storage Regasification Units) and FSUs (Floating Storage Units).

- The LNG fleet grew by around 6–8% year-on-year, keeping pace with global trade growth, which increased by roughly 2–3% in 2024.

- This balance between fleet expansion and trade growth reflects a stable shipping market supporting global LNG distribution.

*Source: International gas union ( https://www.igu.org/ )

The COP 26 summit (Glasgow 2021)

The world agrees to phase-out fossil fuel subsidies and reduce coal

Nearly 200 countries at the UN climate change summit in Glasgow have committed to revisit and strengthen their 2030 emissions reductions plans, keeping the door open to 1.5°C temperature goal.

It is certainly not enough. But this is a process.

Accelerating the transition from coal to clean power.

A just transition to clean energy and the rapid phase-out of coal has been at the heart of the COP26. More than 40 countries have committed to shift away from coal including Indonesia, Vietnam, Poland, South Korea, Egypt, Spain, Nepal, Singapore, Chile and Ukraine. Countries also committed to scaling up clean power and ensuring a just transition away from coal.

Strengthening emissions targets: The Climate Pact signed at COP 26 will speed up the pace of climate action. All countries agreed to revisit and strengthen their current emissions targets.

LNG is a bridge between fossil fuels and renewable energy.

”By generating 30% less carbon dioxide (CO2) than fuel oil and 45% less than coal, LNG is regarded as the ”cleanest” fossil fuel. With natural gas use expected to account for 25% of the world energy portfolio by 2035, LNG is seen as an ideal energy alternative to help reduce greenhouse gas emissions and to bridge the gap between more harmful fossil-based fuels and future sustainable technologies such as hydrogen.”

LNG can service as a backbone of stable energy production while markets build their investment in renewable.

People and countries must act Today with an efficient and realistic energy transition plan in order to save our Planet for Tomorrow.

Sources:

https://ukcop26.org/

https://www.gasworld.com/karpowership-cop26-and-lngs-role-in-the-energy-transition/2022174.article

Canadian Resources and Information On Natural Gas

- Canadian Association of Petroleum Producers – www.capp.ca

- Canadian Centre for Energy – www.centreforenergy.com

- Canadian Energy Research Institute – www.ceri.ca

- Clean Air Strategic Alliance – www.casahome.org

- Energy Resources Conservation Board – www.ercb.ca

- Environment Canada – www.ec.gc.ca

- Learn more about LNG – https://gasmobility.totalenergies.com/insights/downloads